Winston Churchill is said to have remarked that the American people can be relied upon to do the right thing, but only after trying everything else. It is a statement of both enormous faith and biting criticism by perhaps the greatest friend America has ever had and the person arguably most responsible for delivering the world through the convulsions of World War II and into the “rules-based system” that America led from then until maybe the present time.

We have a president in Donald Trump who believes that system was unfair to the United States and who set out early in his second administration to radically change it. The story of the past year in financial markets was about how those changes, most notably imposing radically higher tariffs on US trade partners, were first expected to affect, and later were revealed to affect, all manner of assets—stocks, currencies, sovereign debt—as market participants worked out their calculations of the consequences of policy changes on economies, corporate earnings, governments finances, etc.

A Year of Disruption on the Way to Rewards. As you may remember, the initial reaction of the US stock market to President Trump’s “reciprocal” tariffs was shock. The S&P 500 had already retreated 10% heading into the announcement and proceeded to drop another 10% in the next few days. From that point forward, a sequence of backpedaling, reprisals and exceptions ensued as the President reacted to market signals and countermeasures of our trading partners.

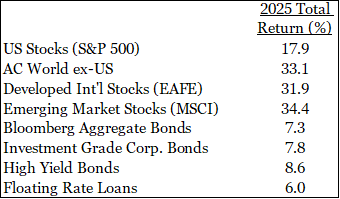

However, our clients were prepared, from an allocation point of view, for the disruption and generally experienced far shallower declines than major market indices. That preparation came from deliberate and mixed investment policies of both stocks and bonds and, within stocks, from significant allocations to foreign stocks which suffered substantially less than US stocks in the sell-off and went on to handsome returns for the year as shown in the chart below. Even US stocks recovered and had a rewarding year based on the remarkably durable nature of the economy and the ability of companies to adapt to the evolving situation. Bonds also did well during the year due to substantial yields and generally declining interest rates.

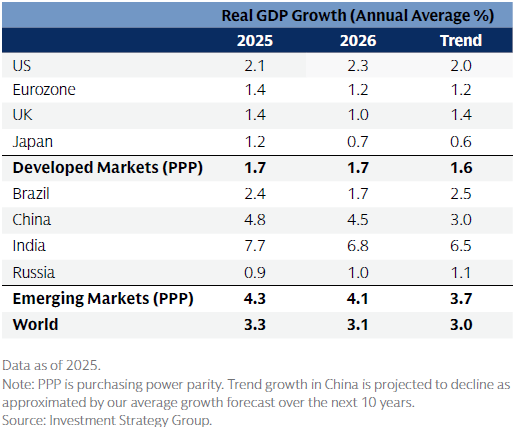

While these results were quite positive for owners of financial assets such as our clients, we are mindful that the economy is very different for many lower income Americans. The financial press refers to this as the “K-shaped economy,” a bifurcated environment where asset owners feel room to spend while lower income people suffer disproportionately from inflation and have greater difficulty finding work. This represents an element of fragility in the economy that bears watching. Nevertheless, economic growth is expected to pick up somewhat in the US in 2026 on the basis of limited US fiscal stimulus and lower interest rates. Below is Goldman Sachs Investment Strategy Group’s economic forecast for the US and major developed country regions for 2026.

Looking Forward and Overall Portfolio Positioning. The US stock market, particularly for large company stocks, has been expensive for a long time, the concentration of stock leadership in the US is a point of fragility and many deep value opportunities lie in smaller company stock and elsewhere in the world. Our response to this environment remains to mix both large and small US index and non-index funds together with international stocks and a client’s bond allocation so as to participate in the advancing market while being cushioned from the full volatility of downward moves. Where we have evolved is in reducing concentrated managers whose fees are substantial and who may miss the few stocks that can sometimes lead the market higher in favor of inexpensive, index-like factor approaches that capture most of the market, yet with tilts that should benefit investors over long periods. We’ve also looked for additional yield in bond allocations, where we think that can be done without risk to the allocation’s ability to provide buying power when stocks decline. We expand on the push-and-pull nature of these crosscurrents in the paragraphs that follow.

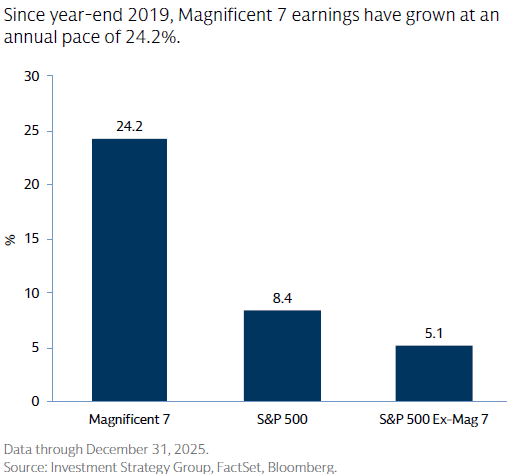

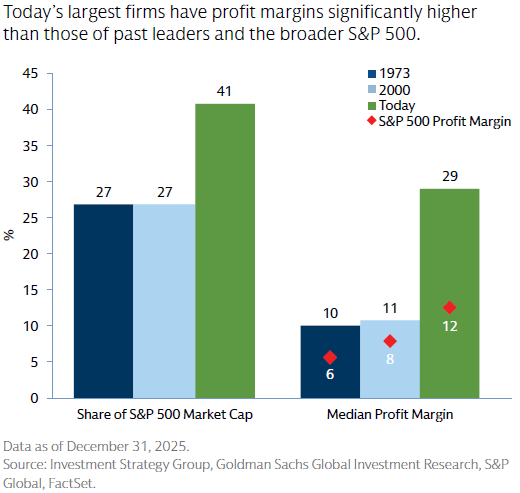

Characteristics of US Stock Leaders. While the US has many economic advantages compared to other countries, to the extent that US corporate earnings are concentrated in a small number of extraordinary companies, there is additional risk around aggregate S&P 500 Index earnings if the circumstances that gave rise to such firms’ profitability are ultimately transitory. As you can see in the charts below, the so-called Magnificent 7 tech stocks that lead the US market have grown almost five times faster than the rest of the US market, in part due to profit margins that are much greater than market-leading firms at other times of high US stock index concentration.

In other words, while Mag 7 stock prices are historically stretched, their leadership may be at least in part justified by meaningfully greater earnings growth, in contrast to prior periods (e.g., Tech Bubble). That said, certain of the Mags (e.g. Nvidia) seem vulnerable to profit margin compression from future competition and so may be “over-earning” presently.

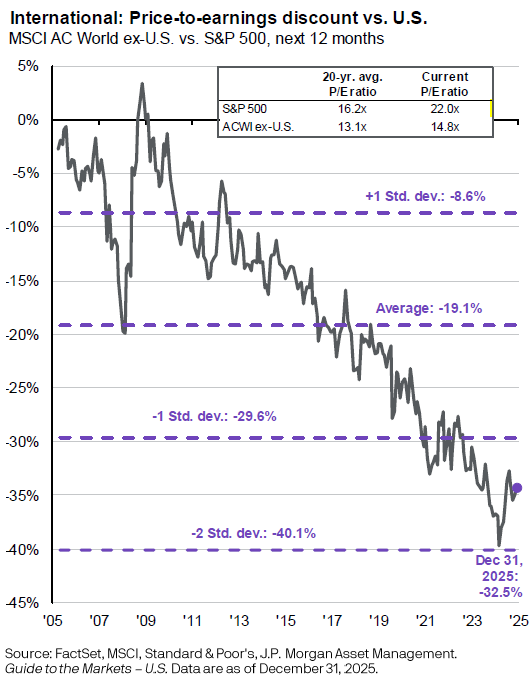

Continued Value in Foreign Stocks. Currently, foreign stocks have risen off their greatest discount to US stocks, measured by price per dollar of earnings, and probably have room to improve further considering increased European spending, heretofore underweight allocations to foreign stocks and general dollar weakness.

The “Sell America” Theme. Moving forward, one message we wish clients to remember is that they remain prepared for an uncertain pathway in financial markets and that radical adjustments in their portfolios in response to events of the past year are probably unwise. We are thinking in particular about clients who may be so upset by recent events that they believe they need to dispose of or radically reduce their ownership of US assets. While actions both at home (e.g., immigration policy) and abroad (e.g., trade policy) have consequences for the United States that we believe are mixed at best, the advantages of the United States in terms of sheer scale of our companies, returns on investment capital, technology generation and other factors persist and mean that the United States remains in many ways the most desirable destination for capital. As mentioned above, clients already own substantial amounts of non-US companies, so the need to diversify from the US is not the same as it would be for an investor who has only owned US stocks and realizes that he or she needs to diversify.

Our caution above stems from the prevalence in the press of the “sell America trade,” and so it is worth exploring this idea for a bit considering the relevance of international portfolio investment flows. The phrase gained prominence in the wake of President Trump announcing “reciprocal” tariffs on friends and foes alike. To paraphrase global geopolitical analyst Ian Bremmer: The old deal that the US offered its allies was, “We’ll defend you and buy your stuff and in return you buy our bonds and invest in our economy.” But now, maybe the US doesn’t defend its allies and wants to keep some of their goods out of the country, so it follows that our trade partners might accumulate fewer dollars to invest in the US and be reluctant to do so in any event. There was much talk of the sell America trade immediately following Liberation Day, and one could observe the dollar declining in the months following. Just this January, certain Danish pension funds resolved to sell their US Treasury holdings following President Trump’s seeming threat to take Greenland by force.

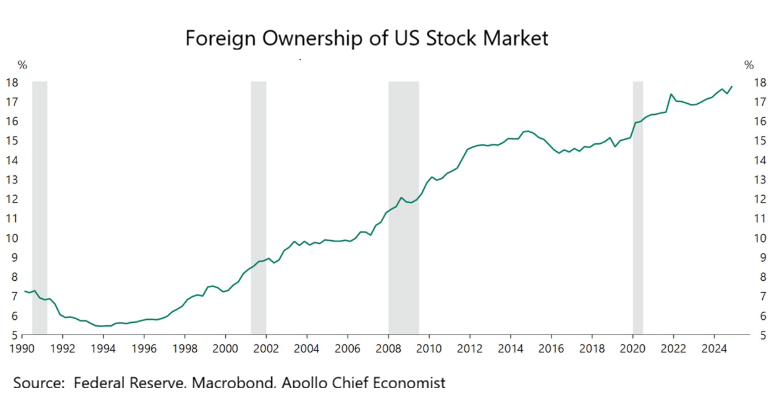

Should foreigners choose to sell US stocks at scale and with speed, we would expect to see a dampening effect on US stock prices given the degree to which foreigners have accumulated US stock investments, as shown below. (Foreigners also own about 35% of US Treasury debt, which is a topic for another day.)

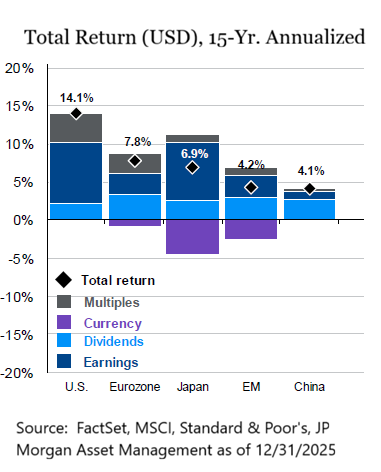

That buildup of foreign ownership has been understandable considering the US current account deficit (which leaves foreign firms with dollars to sell as a result of trade flows) and because profits that US firms have generated since the Global Financial Crisis have generally been the strongest compared to other regions as shown below. Currency changes during that period have favored dollar-based assets (see the effect of the purple shading detracting from returns for foreign stocks). That effect could be very different moving forward. (Note: “multiples” means the portion of return from stocks that can’t be explained by improved corporate earnings or a dividend but just from stock prices going up.)

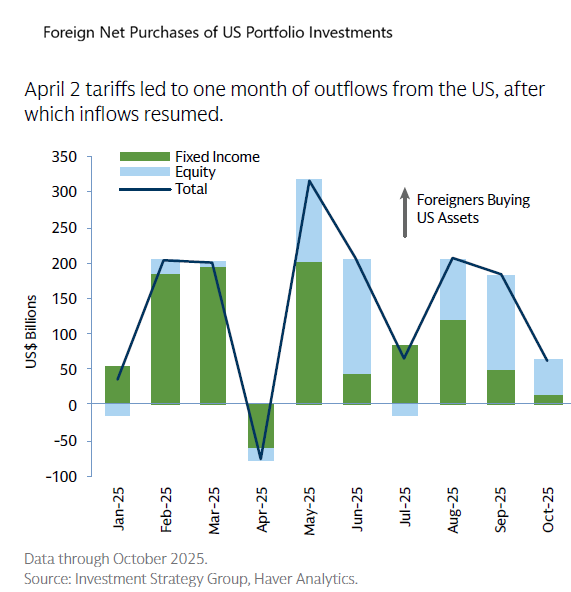

At least in 2025 one can observe in the chart below that the sell America trade never really took hold, in that only April registered a net sale of US portfolio assets by foreigners. Instead, the dollar’s decline was affected by foreign investors starting to hedge the currency exposure of their US investment positions. Foreigners had been accumulating unhedged US investments since the Federal Reserve began raising interest rates in 2022, which raised the cost of hedging to uneconomic levels. When tariffs were imposed, foreign investors started to question the currency exposure of their dollar assets (i.e., US stocks) and bought currency hedges that were then less expensive because the Fed had started cutting interest rates. All of that hedging in the currency market drove the dollar lower against most major currencies.

One concern hanging over US financial markets and the dollar has been the question of who would succeed as Federal Reserve Chairman when Jerome Powell’s term ends in May of this year. The independence of the central bank has never been perfect but is a pillar in our capital markets and President Trump’s attacks on the Fed in this second term have been extraordinary. The selection of Kevin Warsh, while much discussed some time ago as a distinct possibility, is something of a surprise. Warsh, who clearly has signaled an interest in dropping interest rates (no one was going to get the job without that), also has been a vocal critic of the Fed’s past “zero interest rate policy” and balance sheet expansion in the decade after the Global Financial Crisis, policies that have contributed to wealth inequality in the United States.

All told, we expect the “sell America” theme will persist in the press for a while, at least for so long as US administrations persist in upsetting arrangements with our allies and trading partners. Given the advantages of US companies, it’s hard to see more than a modest rebalancing toward home country companies coming to pass in the near term, even if the US becomes a less attractive place for investment over a long period due to changes to our economy and institutions. The US capital markets have already experienced with no obvious effect the disappearance of “petrodollars” from net oil imports (which peaked at $327 billion or 2% of US GDP in 2011) that were recycled back into US assets prior to the boom in shale fracking making the US a net oil exporter. Nevertheless, the phenomenon bears watching and at a minimum is an element in the negative outlook for the dollar (and positive outlook for foreign stocks) over the next few years. Even so, with substantial holdings of foreign stocks, clients should benefit on that side of their portfolios if flows move in that direction.

While this letter has been devoted to explaining the large change in US vs. foreign stock performance in 2025 and prospects for 2026, we should also mention that the bond market offers reasonable absolute returns in the form of current yield, even if the additional yield over US Treasuries for corporate bonds (i.e., “spreads”) are thin. That is due to a combination of strong demand for bonds, the healthy state of corporate borrowers in general and the more challenging fiscal position of the US government. These dynamics are worthy of greater exploration but need to await our next letter.

We know that the intersection of the economy, politics and your portfolio can often feel disjointed, but rest assured, we think our client portfolios are well positioned to weather what could be another volatile year. We continue to meet with your portfolio managers on a regular basis, watch and assess the effects of the economy and politics on your holdings, and reach out for approval when changes are warranted outside of your normal review cycle. As you have personal changes to your risk appetite, needs for cash or other life events, we hope you will reach out to us.

Finally, we are mostly settled into our new office space at 1201 Western Avenue, and are enjoying the pleasant neighborhood, better building management, easy access to lots of eateries, and of course the wonderful view. We look forward to having each of you in the new space soon.

As we pick up the pen to share our reflections on the investment environment, our task is to give context and a sense of direction for our approach to managing client investment portfolios amidst increased investor anxiety (measured by mainstream press stories) about the high price of US stocks and whether the pullback reflected in markets in the last days as this letter goes to press is the start of some larger event. While we can’t predict what markets will do in the next day or even in the next year, our task is, and has been, to help clients prepare for how the current environment shapes the probability of investment returns for a variety of assets rolling forward over several years.