We shall not cease from exploration, and the end of all our exploring will be to arrive where we started and know the place for the first time. -T. S. Eliot

Come along! Hop up here! We’ll go for a jolly ride! The open road! The dusty highway! Come! I’ll show you the world! Travel! Change! Excitement! Ha ha ha! -J. Thaddeus Toad, Esq. (in the 1949 film The Adventures of Ichabod and Mr. Toad)

Reflecting on the path of financial markets in the second quarter—an extravagant round-trip of sorts in US stock prices—brought to mind the above quote from Eliot about coming back to where we started. The attempt at sober reflection for your author is also permeated by a kind of surrealism when seeking to make sense of the traveled path of economic policy changes announced during in the quarter and the market’s reaction to them. The whole business resembles the careening turns of Mr. Toad’s wild ride.

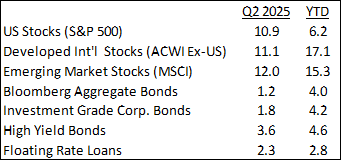

And yet, something of Eliot’s knowing a place for the first time resolves from the exercise: In experiencing the swift retreat in US stock prices in the wake of President Trump’s “Liberation Day” tariff announcements, investors with globally diversified portfolios saw illustrated the utility and wisdom of investing not just in US stocks, but also in companies beyond US shores, as evidenced by our clients’ material outperformance of the S&P 500 index during the February to April downdraft. Foreign stocks held up much better during the quarter and are significantly outpacing US stocks year to date as shown in the chart below.

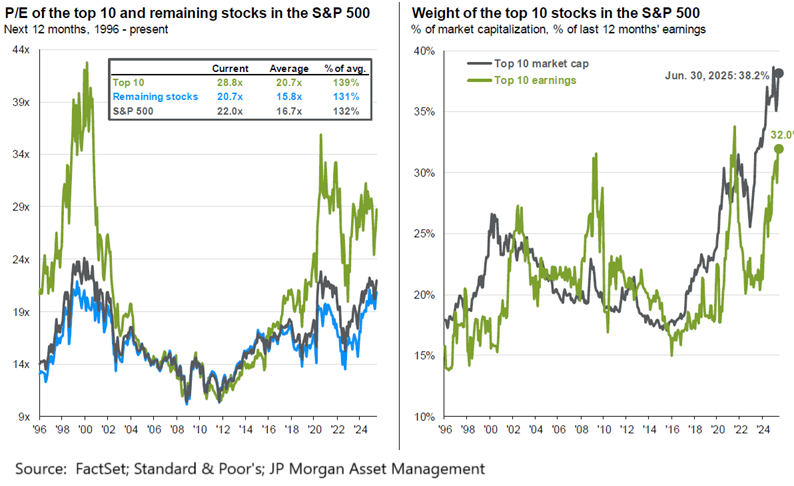

The sense of returning to where we started isn’t just that US stocks have recovered and gone on to newer highs; that’s normal in the long run, although potentially premature as the effects of tariffs and deportations work their way through the economy. (More on that below.) It’s that the US market is back nearly to its prior level of concentration in the biggest technology companies and the high pricing associated with those companies.

We have previously described our approach to this situation, which is to have a large allocation to the capitalization weighted index (with its concentration in large technology firms) together with allocations to non-indexed quality stocks and additional equity yield. This overall allocation will trail a briskly rising US market, as was the case in 2024, but should experience less volatility (as noted above) and increase the performance opportunities of the allocation measured over several years.

Policy and Economic Expectations. Returning to the path of policy, it remains to be seen how much the president’s tariffs and deportations will affect economic growth. Initially, prospects were dour, on the order of a 1.5% dip in economic growth just for tariffs. As we contemplated he might do in our letter last quarter, President Trump found it expedient to abruptly change his tariff policy by putting a 90-day stay on his “emergency” tariffs with the view to working out trade deals with other countries. That stay expired July 9, but he effectively extended it to August 1. Meanwhile, the Administration lost in the lower court on the challenges to its authority to institute emergency tariffs using its statute of choice. The US Court of Appeals for the Federal Circuit lifted the lower court stay while the appeal proceeds on the merits, with an en banc hearing of the circuit scheduled for July 31, setting the stage for an accelerated appellate order and eventual appeal to the US Supreme Court. These changes on policy and judicial losses have been priced in by markets, but perhaps without sufficient regard for how policy might change again once August arrives.

In any event, signs of diminution in “hard data” such as consumer and business spending are hard to find, even as “soft data” such as sentiment surveys remain low, albeit off the bottom recorded in the immediate wake of the tariff announcements. Some softness can be seen in consumer dining habits and certain other purchase choices. And while the unemployment rate hasn’t risen materially, it is taking longer for unemployed workers to find new jobs. But inflation data shows less lift from tariffs than expected, and US corporate earnings are still reasonably buoyant and will benefit from the substantial foreign revenues as the US dollar drops. This experience accords with the trend of the last several years, which is that the economy remains remarkably resilient even as economists expect some slowing.

Interest Rates and the Federal Reserve. That resilience has been a surprise to most economists and particularly to the Federal Reserve, which has held its interest rate target steady since late 2024, when economic data seemed to firm up contemporaneously with national elections. President Trump has been vocal and even disparaging in his criticism of Fed Chair Jerome Powell for not cutting rates and has threatened to remove Powell, most recently over the cost of renovations to the Fed’s D.C. headquarters. Powell’s term as Chairman ends in May 2026 and discussion of his replacement will naturally precede by several months. Already, various Fed board members and White House economists have essentially started auditioning for the job by expressing a willingness to cut rates.

This action is damaging to the Fed’s credibility and adds to the challenges facing the longer end of the Treasury bond market, which is already dealing with excess supply from greater federal debt. That damage is counterproductive to the stated goal of lower rates because the Fed’s institutional culture to protect its independence means there will be another reason to defer cuts. The argument over whether to cut rates is a tough one as there has been some weakening in the labor market, and the economy is probably growing around 1%, or substantially below par. At the same time, tariffs have started to have some effect on goods prices, which previously had been subdued and helped bring the inflation aggregates down from the high level caused by persistently high inflation in core services. Powell and others at the Fed are loathe to repeat the perceived mistake of 1970s Fed Chair Arthur Burns, who prematurely cut rates in front of President Nixon’s re-election only to have inflation reignite. And, prior to President Trump instituting tariffs and supercharging deportations, the economy was stronger and seemingly handling the Fed’s rate policy. With the courts potentially only a couple of months from putting the kibosh on the president’s tariff policies and the president backpedaling episodically as deportations cause labor shortages in key parts of the economy, Fed governors may be understandably reluctant to cut rates to deal with the adverse effect of administration policies that may soon hit judicial and political cul-de-sacs.

With this as background, we continue to like our choices with client bond allocations, which emphasize the opportunities away from Treasuries and longer-term bonds and toward securitized credit and various forms of corporate bonds. In all reality, interest rates are likely headed somewhat lower over the coming year, at least for short and mid-term bonds. This will give some lift to the value of all but the shortest-term bonds but eventually diminish return expectations as yields reset lower.

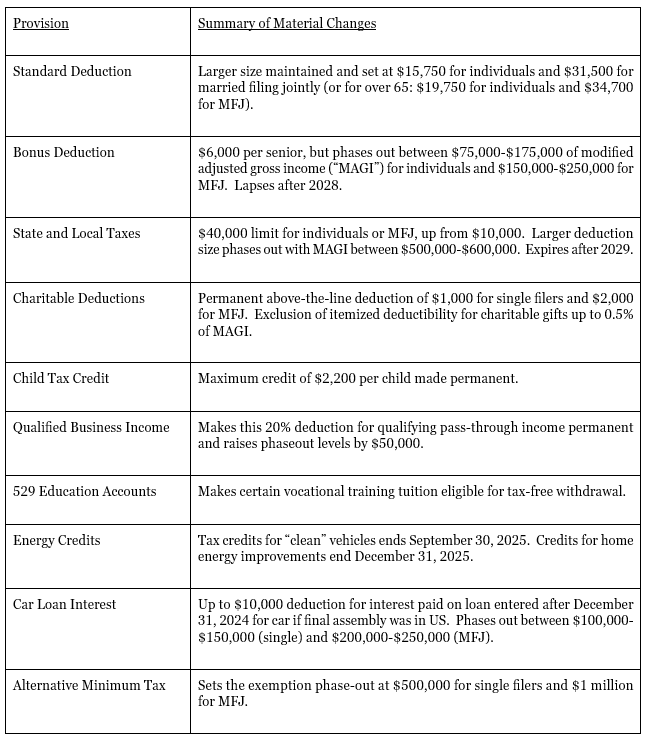

Tax Law Changes. We turn now from financial markets to taxation, with the Trump Administration having achieved its goals of extending the 2017 tax cuts that would have otherwise expired, and adding new cuts, some of which, like no tax on tips and an extra break for seniors (in lieu of no tax on Social Security), were promised during the recent presidential campaign. And for our Washington State clients, the legislature and governor passed changes to the capital gains tax and the estate tax that are material.

The largest effect for our clients of the new federal tax law is to maintain the income tax rate structure of President Trump’s 2017 tax bill, which has its origins in President George W. Bush’s 10-year across-the-board reduction in tax rates and the subsequent renewal by President Obama. Over the years, most of the changes for individuals have been in moving the top two rates up and down by a few points, protecting middle-income filers from the Alternative Minimum Tax, and, in 2017, doubling the standard deduction to where it sits now in exchange for radically limiting the deductibility of state and local taxes paid (SALT). With the 2025 law, the large standard deduction is maintained and SALT deductibility is much increased, although subject to significant limitations as mentioned below.

Summaries of some of the most relevant provisions are below:

Recent tax law changes in Washington State added a second rate (9.9%) for capital gains over $1 million, starting with tax year 2025. Below that level, but above the $270,000 exemption , capital gains are subject to a 7% tax. As a reminder of current law, there is no larger exemption for married filers, and there is no tax on real estate transactions.

Important changes in estate tax law also came out of recent federal and Washington State legislative action. The Trump tax law makes the $15 million exemption per estate (beginning in 2026) permanent and indexes the figure for inflation. In Washington State, the exemption was raised to $3 million and indexed to inflation. The Washington State rate structure was changed to lift rates at the top end; the tax starts at 10% and hits the top rate of 35% on taxable estates of $9 million. Those Washington State changes apply as of July 1, 2025. As a reminder, unlike the federal gift and estate tax regime, there is no gift tax in Washington State, making gifting an important element in Washington State estate tax mitigation.

We hope you enjoy the balance of summer and look forward to speaking with you at the next opportunity. In the meantime, please know we appreciate your trust and confidence in our counsel.