This is the time in the calendar when we write about the prior year and our thoughts about the investment environment moving forward. This year, the timing coincides with us recommending an adjustment across client accounts (separate correspondence about the specifics of trading, if applicable, will follow as needed), so that will be the focus of this letter. In explaining the trade (an increase of investment in US small and mid cap (“SMID”) stocks and corresponding decrease in emerging markets stocks), we seek to also give you some sense of how we got here through 2024 and what we think about 2025 and beyond.

First, as you may already know, the US stock market, as measured by the S&P 500 Stock Index, gave a handsome return for 2024, up 24.5%. Other major elements of client portfolios all had returns in mid-to-low single digits: 1.2% for bonds, 3.8% for developed international stocks, and 7.5% for emerging market stocks, as measured by the respective benchmarks we use. Put these parts together, and client portfolios had solid returns.

Index Concentration, Future Returns and Risks to AI Investment. To deconstruct returns and start to explain our suggested portfolio adjustment, let’s first observe that the returns of large US stocks, as measured by the benchmark S&P 500 Stock Index (the most prevalent capitalization-weighted index for large US stocks), were driven last year to an extraordinary extent by a small collection of leading technology stocks, the most common collection being known as the “Magnificent Seven” (Apple, Amazon, Alphabet, Meta, Microsoft, NVIDIA, and Tesla). The concentration of the US stock market in the value of the largest firms is normal, but it has been getting quite extreme in recent years as you can see in the chart below.

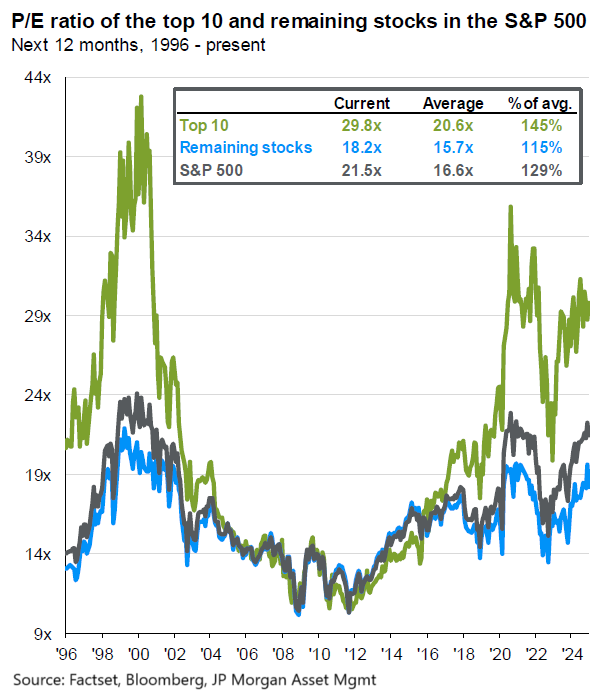

The stock prices of this elite group are high in part because of their growing earnings, but also because of the higher multiple of earnings that investors have been willing to pay for them. Below is a chart showing the price-earnings multiples for the 10 largest stocks in the S&P 500, the index overall and the index without the top 10 stocks. The price-earnings multiple shows the number of dollars reflected in a stock’s price for every dollar of the company’s annual earnings.

As welcome as the performance of US stocks has been the last few years, we need to acknowledge that the high valuation of the index and its concentration in a small number of stocks are both associated with lower future returns, when measured over the subsequent 10 years. To be clear, we can’t provide a forecast for 2025 or any particular year because market phenomena (e.g., seemingly high stock prices) often persist far beyond anyone’s first observation. But the long history of stock prices does provide clues about tendencies once the time period is stretched to as long as 10 years. As we’ve explained before, high current returns are like borrowing returns from the future, and low returns are like banking them into the future.

That concentrated returns should correlate with lower future returns makes sense in that concentrated positioning corresponds with higher volatility because a smaller number of bets means that any one bet can hurt more if it goes wrong. Accordingly, a rational investor should price each bet more conservatively, but when we find excessive concentration in the stock market, prices are typically high (at least among the leading stocks).

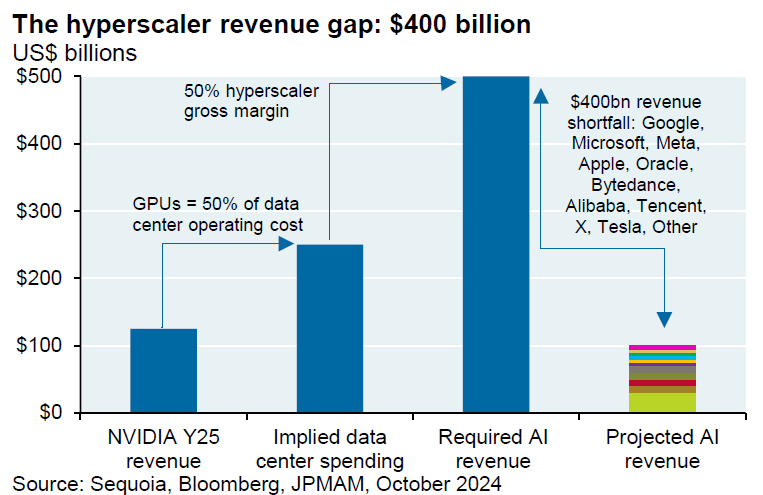

Many developments (e.g., outbreak of conflict; supply disruptions; unexpected inflation) can set the stock market back, but one risk related distinctly to the tech leaders is the possibility that the huge investments in artificial intelligence (in data centers, energy generation to power them and training AI software models to run on them) being made by the leading firms do not result in sufficient new revenue to justify the massive investments. Consider the overbuilding in prior technology revolutions, such as the railroads of the 19th century or the telecom and cable buildout in the early 2000s; the possibility of overbuilding in the AI revolution is considerable. Below is a chart JP Morgan developed to show how the purchase of NVIDIA’s chips is but one part of implied data center construction spending, which then must be recovered with still larger revenues from customer use and finally compared to actual AI revenues.

Despite the expensive nature of the leading US stocks, there is significant opportunity in other parts of the US stock market, in fixed income (debt) investments and in foreign stocks such that the opportunity for meaningful returns over the coming years is quite good.

But for this discussion and our suggested portfolio adjustment, we wish to focus on US stocks and posit that, under the present circumstances, by investing at least some of a portfolio’s US stock exposure without the capitalization weights of the S&P 500 (wherein the largest stocks have the highest weight in the index), one improves the probable distribution of future returns, measured several years out.

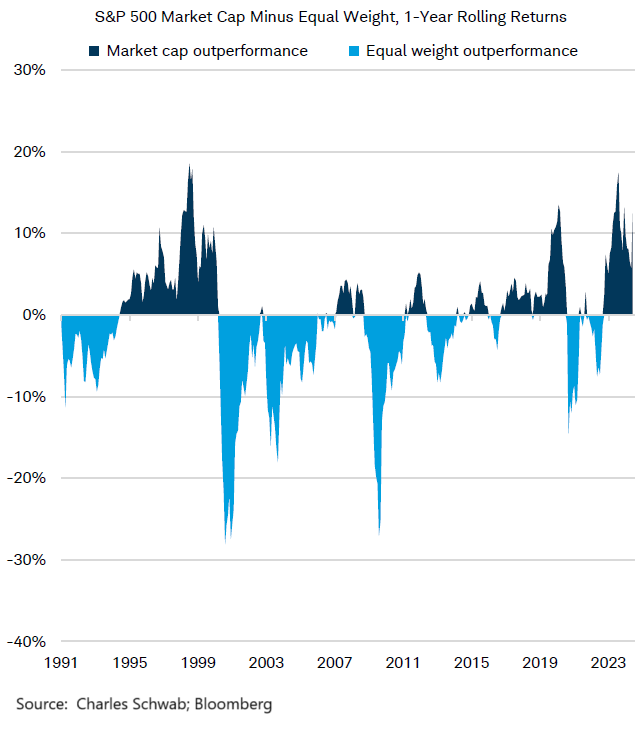

Already, client portfolios typically contain three-fifths of their US stock investment in funds apart from an index tracking the S&P 500 or another major index. With exceptions for growth-stock oriented funds, those investments have largely trailed the S&P 500 the past several years, while still providing handsome returns in absolute numbers. Our approach is to balance index investing and non-index investing among US stocks. We think this is advisable because, although a small number of stocks provide a disproportionately large share of the returns in the US market, it is exceedingly difficult to identify and buy those stocks cheap at the outset, and the psychological nature of the market is to eventually drive the share prices of the leading stocks to excess (typically on the back of a growth narrative such as prevails today with artificial intelligence). When this process culminates in excessive concentration in the top stocks, it sets up a period of outperformance for the rest of the US stock market as shown below in the streaks of outperformance and underperformance for the market-cap weighted index over time.

Opportunity in US Small and Mid Cap Stocks. Not only do we think clients need investments in US stocks apart from the capitalization weighted S&P 500 Index, but we also think the environment is opportune to add to client investments in small and mid cap US stocks. These are stocks that are too small to be included in the S&P 500 and yet, in the format we would choose, have a market capitalization up to $23 billion.

For several years, we have been light on investing in smaller US stocks and that has been to clients’ benefit because rewards to smaller stocks have been significantly lower than large cap stocks, which have enjoyed greater scale, access to cheaper capital, and light antitrust enforcement, among other advantages, resulting in faster growing earnings.

Now, however, those advantages appear to be abating, and small cap companies are expected to experience faster earnings growth than their larger cap peers as shown in the chart below.

Factors contributing to the expected improvement in earnings include falling inflation and interest rates, the lower regulatory burden expected from a second Trump Administration, and the application of AI to improve worker productivity. Although these factors benefit large firms as well, the relief from each of them is more meaningful for small firms. The fall in US small cap stocks since the election of Donald Trump in combination with the Federal Reserve moving more slowly with rate cuts as of December has opened a window to purchase small and mid cap stocks at even better prices than already prevailed before the election.

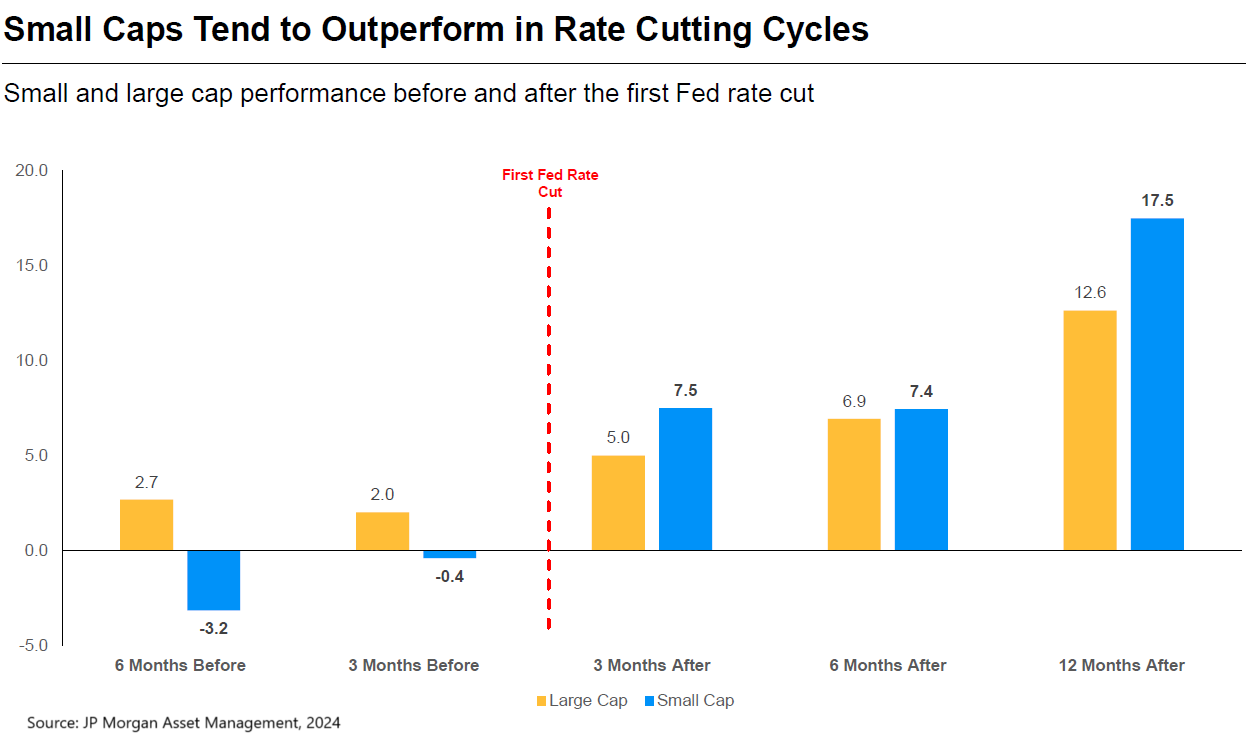

Focusing only on falling interest rates, one can see in the chart below the advantage of small and mid cap stocks over large cap US stocks during the subsequent 12 months following the first cut of interest rates.

Coming Trade Recommendation. For clients where we believe there is an immediate trade to be made, we will be reaching out for approval of formal trade recommendations in the coming days, but wanted to apprise you of this proposed adjustment now as we write about markets.

We hope the new year has been kind to you thus far and look forward to being in touch.

PLEASE SEE IMPORTANT DISCLOSURE INFORMATION AT: KBBSFINANCIAL.COM/NEWSLETTER-DISCLOSURE-INFORMATION/