The US and Israeli attacks on Iran have unsettled stock markets and sent crude oil up over 40% to about $95 per barrel as of our writing on March 9 due to the cessation of significant oil cargoes through the Strait of Hormuz. Clients are rightly concerned about the consequences for their portfolios, to say nothing of the safety of persons in the Middle East and our armed forces.

US stocks so far are off about 3% since the beginning of the conflict through the time of our writing. In the same period, developed international stocks and emerging market stocks are off about 7-8%, highlighting the reliance of major Asian economies on Persian Gulf oil supplies. US Treasury bonds are off slightly as they are pricing in somewhat higher interest rates on expectations for a marginal increase in inflation. While the price of oil for delivery next month spiked to over $120/barrel over the weekend before settling down to about $95 today, longer futures contracts are priced substantially lower, reflecting expectations for easing supply constraints.

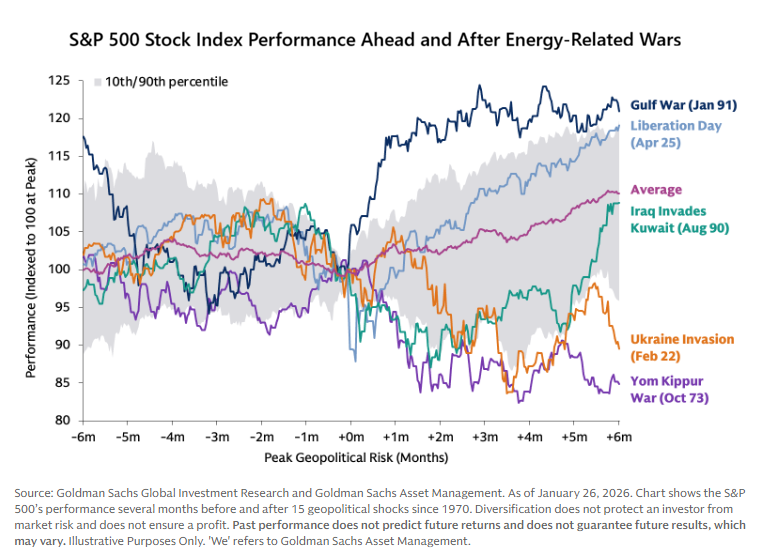

Historical Context for Markets and Military Conflicts. It is important to recognize that as unsettling as military strikes are, there have been quite a number of them over the last few decades and so there is a fair amount of data on their short term and longer term effects on financial markets. In 21 airstrike events since 1986, stocks were up 95% of the time eight weeks out from the start, with a median advance of 4.3%. Focusing on larger conflicts, the chart below developed by Goldman Sachs shows the performance of the US stock market (as measured by the S&P 500 Stock Index) before and after energy-related wars going back to the 1973 Yom Kippur War and ensuing Arab Oil Crisis.

As can be seen in the chart, it typically takes only a few months for the decline in stocks to be recovered. The Ukraine invasion occurred contemporaneously with the Federal Reserve hiking interest rates briskly to suppress the inflation that had set into the economy following the Covid pandemic. So, the adverse path of stocks in that episode should be largely attributed to non-geopolitical factors.

The Outlier of the Yom Kippur War. In the table above, the big adverse outcome shown is from the Yom Kippur War, which was followed by a long period of restricted oil supplies as Arab countries objected to the US supplying key arms to the Israelis in the conflict and significantly curtailed shipments of oil to the US. Oil prices quadrupled within three months of the conflict. Your author was too young to drive at the time but has clear memories of sitting in the back seat of the family car for long periods while his parents queued for gas.

The role of oil in the US economy is radically different today compared to then: now the US is a net exporter of petroleum, obtains a significant fraction of energy from renewables and is vastly more efficient in the use of energy per unit of economic production. That said, oil is a global commodity, so US businesses and consumers are not insulated from the effects of global price changes and the follow-on effects to the economy generally, although the drag on growth is mitigated by higher prices obtained by domestic oil producers. As well, hydrocarbons are major inputs in fertilizers, which are significant contributors to crop yields. With fertilizer shipments through the Strait also suspended, tight supplies will affect food production and prices down the road.

Some mitigation of the supply squeeze is underway. The US Treasury has given India a temporary reprieve of sanctions for the purchase of Russian oil. Major oil consuming countries are discussing the release of strategic oil reserves that were developed for just this type of situation after the experience of the 1970s. Commercial stores of oil were high prior to the outbreak of hostilities. Saudi Arabia and the U.A.E. can reroute some supplies to ports on the Red Sea and Gulf of Oman. President Trump has mentioned using the Export-Import Bank to provide marine insurance and having the US Navy escort vessels through the Strait, as was done for a time during the Iran-Iraq war; however, neither of these measures are underway as we go to press.

Considerations on Duration. How long the Strait of Hormuz stays closed is very difficult to say, and that is the key factor in the price of oil. Currently, markets seem to be pricing in a few more weeks. A longer closure risks actual shortages and more serious economic fallout.

The duration is made more difficult to judge by inconsistent statements from the President and other administration officials about the objectives of the war. The President has tended to personalize the conflict and phrase the goal as the collapse of the Iranian regime, something without historical precedent on the basis of aerial bombardment alone. The Pentagon has stressed the objectives of significantly curtailing Iran’s missile, drone and naval capabilities so that it is a reduced threat to regional peace. The US and Israel have significantly slowed the pace of Iranian missile and drone launches by destroying launching equipment, launch sites and stockpiles, showing progress towards Pentagon objectives. Yet, the Iranians are reputed to have a large remaining supply of inexpensive, slow-flying drones, which remain a threat to shipping.

In this contest of wills, the two sides have large incentives to find a means of deescalating. Iran needs to make oil deliveries to fund its economy. President Trump has been sensitive in the past to financial market pressures and has long complained about extended military engagements.

Conclusion. What we can say is that there is a high degree of likelihood that investors will be rewarded in the medium to longer term for maintaining their investments. Thus, making a move now to reduce investments, particularly stock investments (something that occupies the press in a crisis), would be a risky bet that markets will continue to deteriorate and that the investor can buy back before they recover. Such market timing exercises are very difficult to execute successfully and are just inherently unnecessary given the longer experience of markets. And, if a pronounced stock market retreat comes to pass, clients are prepared with mixed investment policies of stocks and bonds that represent stores of durable assets that can be trimmed to purchase additional stocks in a downturn. As well, we have allocated clients on the stock side in a manner to reduce exposure to the most expensive, largest companies that represent additional risk in a market retreat.

It is also worth mentioning that this oil shock is arriving to a global economy that has been performing rather well for investors based on statistical measures rather than anyone’s personal experience. For example, the US economy grew about 2.2% in 2025 and is expected to gather pace in early 2026 due to federal fiscal stimulus and the refund of past tariff payments. Remarkably, the economy grew without adding many new jobs. This is due to labor productivity growth of 2.8%, much above the post-Global Financial Crisis norm. So, while hourly compensation rose 4.1% last year, due to productivity gains, company costs of employment rose only 1.3%, contributing to corporate earnings that grew 14% for the S&P 500 in the fourth quarter.

Like you, we find the war in the Persian Gulf discomfiting on many levels. We hope the context provided by this letter is helpful. If you need to better understand your financial picture in light of events, please don’t hesitate to call.