By now we have all heard the saying that “the enemy gets a vote” in any war. But you know who else gets a vote? Financial markets.

We mention this because the current and prospective path of the markets as a kind of referendum on the Iran War is seemingly much on everyone’s mind. Like watching election returns late into the night, we have a sense that many people are looking for the US stock market in particular to reinforce their opinions on the conflict itself.

Early on in the war, we wrote that the stock market tends to look through geopolitical conflicts as near-term disruptions in a much longer and more significant stream of earnings from the future beyond the event. Thus, the magnitude of harm that the world experiences in the event far outweighs the impairment of the stream of earnings, creating a kind of cognitive disconnect between how we perceive the event and how that event is reflected in financial markets.

None of this is to diminish the uncertainty surrounding the future of the conflict. The range of potential consequences for the global economy and financial markets still seems quite broad even as stock and oil prices at any particular time reflect a collective judgment rendered as a single price (e.g., the value of the S&P 500 Stock Index, or the spot price of a barrel of oil). Markets may be undervaluing the damage being wrought by the disruption of about 10% of global oil supplies and expecting too quick a resolution.

President Trump is famously fond of deals, but his negotiating counterparties, the leadership of the Iranian Revolutionary Guard Corps, have a seeming tolerance for adversity developed in the grueling and costly eight-year Iran-Iraq war. Thus, the likelihood of a deal of any sort that’s consonant with the president’s stated goal of a de-nuclearized Iran seems distant. If anything, it seems we are more likely to face a test of the current nominal ceasefire and blockade where Iran seeks to break out of the stranglehold by renewing pressure on oil prices using additional attacks on Persian Gulf neighbors and ships attempting to transit the Strait of Hormuz.

How this ends is very difficult to say. In fact, it may turn out that an ending in a traditional sense is tough to spot, but instead what resolves by slow turns is an uncomfortable accommodation to periodic conflict, permanently reduced traffic through the strait, tighter sanctions on Iran (if not an actual blockade) and increased construction of infrastructure to move petroleum and related products without use of the strait. This situation in the Persian Gulf is one more example (others being Russia’s invasion of Ukraine and trade limitations on semiconductors) of how geopolitical issues are affecting supply chains and the cost of physical goods. More on that, including the sometimes seemingly incongruent investment backdrop, further below.

First Quarter Results Reinforce Strategy. The war has had the effect of displacing attention on other financial themes and trends. It is worth revisiting these as they remain relevant to the economic and financial backdrop and our approach to managing client portfolios. Here are a few highlights from the quarter that ended March 31:

- World stock markets (ex-US) advanced slightly in local currency terms and were off less than a percent in US dollar terms, ahead of US stocks (down 4%).

- Within US stocks, large value stocks (up 2%) outperformed growth stocks (down 10%), with the so-called Magnificent Seven growth stocks (Alphabet, Amazon, Apple, Meta, Microsoft, NVDIA and Tesla) down 11%.

- The best performing part of the US stock market was small cap value stocks (up 5%), followed by mid cap value (up 4%).

These outcomes buttress our view that clients are served by having a mix of US and international stocks in portfolios and some significant weighting away from the concentrated parts of the US stock market (currently, large growth-oriented companies). And, although our move to add to small cap stocks in the Spring of 2025 didn’t provide early rewards, we are pleased with the outcome as measured over the period since then.

These favorable results in the stock market are supported by an economy that is generating strong earnings growth for companies beyond the large technology firms. The median company in the S&P 500 Stock Index had year-over-year earnings growth of 10% in the first quarter. Large technology firms recorded even faster growth, but that comes with questions about whether those earnings are sustainable long-term, a topic we’ve addressed in prior letters.

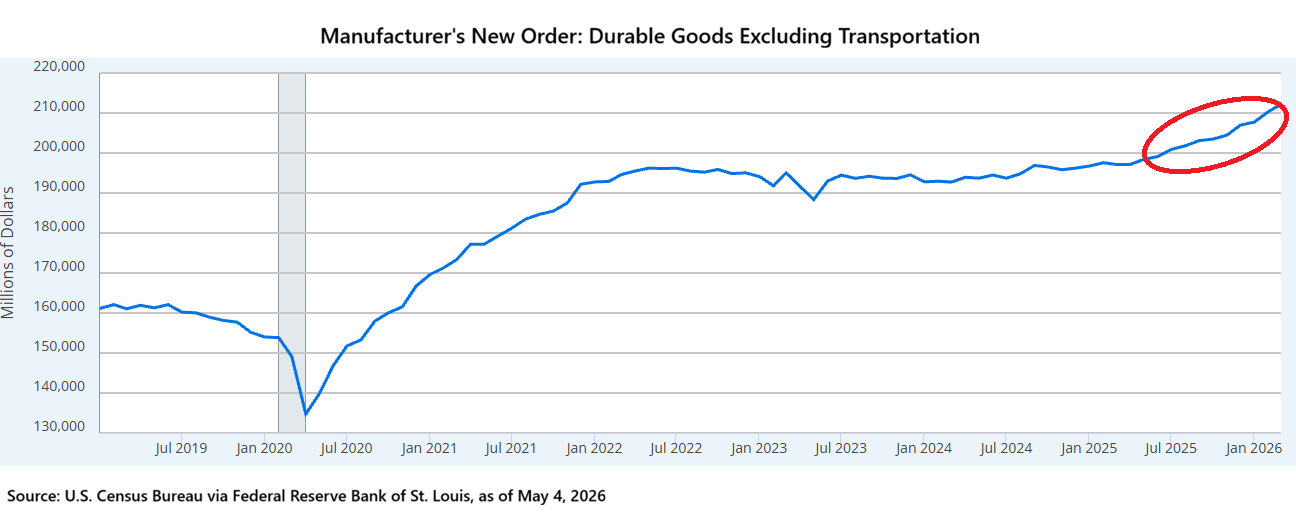

Manufacturing Moving Up. Two recent charts caught our eye for the peek they give into a potential shift toward momentum in manufacturing, which had seen tepid growth over the last several years. As shown below, manufacturer’s new orders (excluding transportation; autos cloud the data) have been trending up markedly since the Spring of 2025. Manufacturing is a minority share of the economy compared to services but tends to play a leading role in the business cycle, so the uptrend has significance.

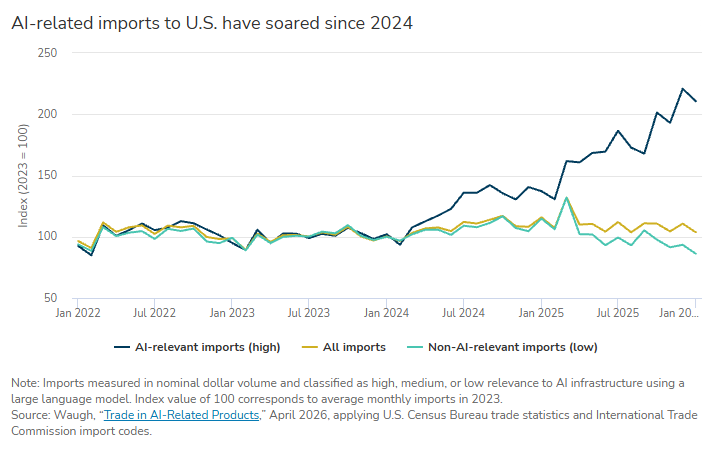

Next, during the same period and for a bit longer, imports of AI-related electronic equipment have been rapidly advancing, while imports of all other goods collectively are on the decline.

This chart and the preceding one are interesting as evidence of some shift in supply chains back to the US, even as the hottest sector of business investment (building data centers) requires an enormous amount of equipment from overseas (largely microchips fabricated in Taiwan). This chart also helps debunk, with the aid of some economic math, the oft-repeated claim that the economy wouldn’t be growing without data center construction. In truth, because 75% of the cost of data centers involves foreign sourced equipment, and imports are subtracted from gross domestic product, data center construction has had a negligible effect on measured GDP growth. For reference, GDP growth was 2.0% in the first quarter, up from 0.5% in the fourth quarter of 2025.

Looking Further Out. More generally, it seems to us that physical goods and the capital to make them are increasingly important to the US economy (or at least issues about obtaining and controlling them are increasingly important), whether robotics to deal with our demographic problems and improve productivity, or the need to bring home or at least move to friendly countries manufacturing of components critical to the economy (e.g., semiconductors; rare earth minerals), to say nothing of the resources necessary for the data center buildout to support artificial intelligence services (like ChatGPT and Claude). If tangible products will have greater relevance to the global economy than in the “digital revolution” that emphasized software services, then we make the following observations:

- Lowest cost of production will not always control supply chains for products as disruption during Covid and competition with China have laid bare US vulnerabilities. This creates upward pressure on prices and interest rates (i.e., rewards to lenders) as a consequence.

- There is a greater need for capital to produce goods and even to build the data centers and supporting power generation to deliver the AI-enabled software services of the future.

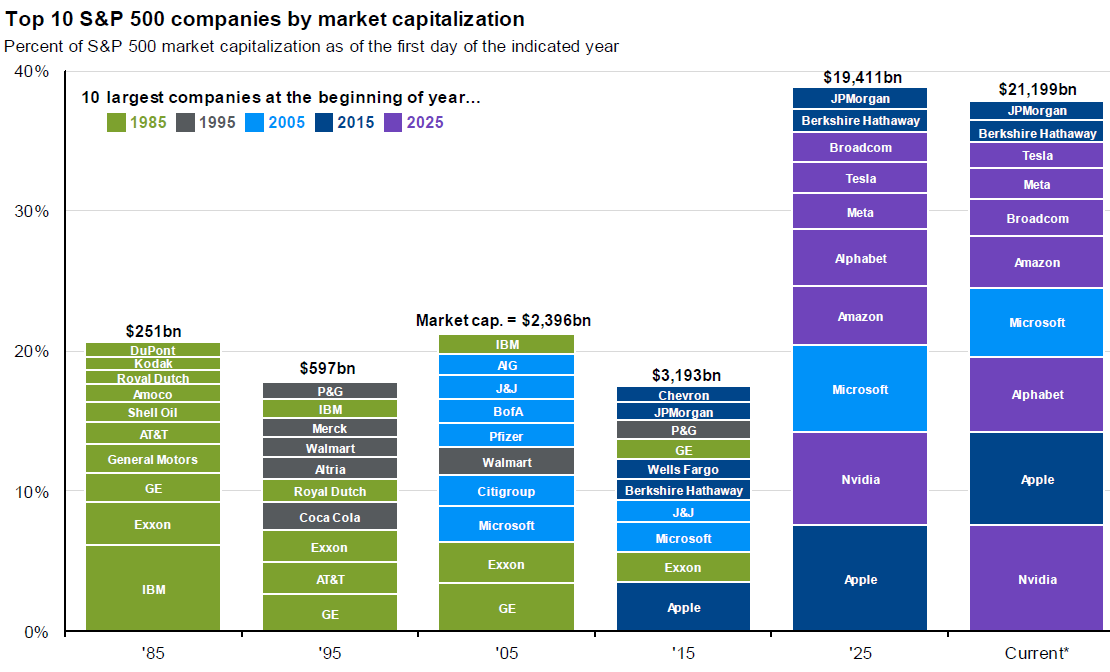

- This major adjustment in the economy bodes for an evolution in the leading companies even if today’s top tech firms are not going away. This process of changing leadership among top stocks is always at work as shown in the chart below. To make sure our clients participate in this evolution, investment in a broad equity index, as is present in our investment models, is critical.

Reflecting on these observations, we think the consequences for investors are generally favorable. Greater demand for capital doesn’t guarantee better returns, but does put upward pressure on bond yields (which would increase income on client bond investments over time). Any related adjustment in equity prices (i.e., a rise in bond yields tends to put downward pressure on stock prices) should hopefully be recouped in greater productivity obtained through the current AI-led revolution in product generation and delivery.

Private Credit Shakeout. One area of investment that’s been rewarding, private credit, is much in the news as some retail investors sort through their long-term commitment to the space and the realities of the structures available for them to invest in it. Private credit is mostly composed of direct loans made by non-depository firms (historically, firms that got started doing buyouts) to significant private companies. These companies typically have annual revenue of $100M or more and may be family-owned but are more likely controlled by private equity investment firms. As the public markets have become more and more inaccessible and banks have had to retreat from corporate lending due to regulatory strictures, private credit lenders have become the go-to solution providers of debt finance for large private companies. For investors, private credit has been a valuable place to invest as yields tend to be 2-3% above the public, high-yield debt market, while defaults and recoveries historically have been more favorable.

Traditionally, private credit firms obtained capital from institutional investors using limited partnerships where capital is drawn down over several years, invested and then returned to the limited partners as investments are sold. We have used this structure in a limited way, and it is tedious and available only to the largest clients. It continues to represent about 85% of capital in the private credit space. Beginning a few years ago, private credit lenders started creating perpetual (“evergreen”) funds, some of which are private and have investor-qualification thresholds and others that are purely public. To protect the funds from having to quickly dispose of a significant share of assets, the funds limit aggregate redemptions among all investors to no more than 5% of the fund’s assets in any calendar quarter.

We have recommended such funds (by Oaktree and Apollo) when appropriate for a client’s portfolio and believe they remain valuable contributors to the clients that hold them. The funds have lower leverage and substantially lower non-accrual loans than their peer funds, befitting the managers’ value-oriented, conservative approaches. As described in our reports and materials to clients, our method has been to recommend these investments where clients understand and can handle the liquidity limits and where we look to generate higher returns on a fraction of the client’s bond holdings that are not needed for rebalancing against stocks or to see a client through a period of stock market decline.

As with any new investment area, enthusiasm often becomes excessive and some event is needed to shake out the excess. In this instance, the cause of concern is whether alternative intelligence (AI) models will displace software sold to businesses. Such software firms constitute about 25% of the private credit borrowers generally, less so in funds we’ve recommended. Debate on this topic is unsettled, but it is fair to generalize that there will be winners and losers among companies. Thus far, there has not been widespread cancellation of software subscriptions, and defaults in private credit remain subdued. Nonetheless, some investors in evergreen private funds are taking a “shoot first, ask questions later” approach and are seeking redemptions that have exceeded the 5% limit for most major evergreen private credit funds.

The Oaktree fund we have used is one of the rare such funds that satisfied redemption requests in full for the latest quarter (their requests for redemption were not far above the 5% limit and they used an investment by parent Brookfield for the excess). The Apollo fund, like most such funds, limited aggregate redemptions to 5% for the quarter just ended. Meanwhile, clients continue to receive dividends of 8.5% and 8.1% from the Oaktree and Apollo funds, respectively, which are fully earned from interest on the debt holdings of the funds. As mentioned, we recommend continuing these investments and are glad for their role generating higher income for a more or less permanent portion of a client’s bond holdings. Given the modest size of allocations we’ve recommended, we do not anticipate any material difficulty rebalancing client portfolios while fund redemptions run above the 5% limit.

We expect net redemptions in evergreen private funds to continue through 2026 and for the process to result in better interest rates for private credit firms and their investors as inflows to the space slow down. Indeed, private credit firms continue to raise capital through traditional partnerships from institutional investors, and several firms have recently raised new partnerships for purchasing loans they expect evergreen private funds to need to sell to meet redemptions.

* * *

For news on the firm, we have recently hired Cindy Garcia as our principal trader. She comes to us after several years at another independent advisor and a large institutional investor. Cindy’s arrival is timely in that colleagues Austin Jodrey and Ashlyn Wallace will take parental leave for portions of this year as they welcome new additions to their families. We will communicate more about those developments in the coming weeks.

Please let us know if you have questions about this newsletter or any other need to discuss. We hope you are enjoying a lovely spring and look forward to seeing you or hearing from you soon.