Dear Clients and Friends of the Firm:

In looking back at the year, as we always do in our customary January newsletter, the Covid-19 pandemic was obviously the big event, and it caused a cascade of subsidiary effects, some of which will have enduring consequences for our economy, and investment and financial planning, as we summarize in this letter.

Covid qualifies as a “black swan” under a definition given by Nassim Taleb in his well-known book of the same name: a rare event that is extremely impactful and predictable in retrospect. Perhaps surprisingly, Taleb admonishes us not to predict rare events (they’re random!) or seek to profit from them (very difficult to execute!). Rather, his argument is that random events with big consequences are a dominant force in human existence, and we would do well to fashion ourselves and our institutions to handle them better when they come. We won’t dwell here on Taleb’s idiosyncratic book, which we recommend as a challenging and entertaining read, but remark only that his key advice accords with our belief that uncertainty is a profound feature of investing, and our job as financial counsel is to help clients stay secure no matter what the future brings. Included in our review below are some notes on how we do that, as well as a description of adjustments we’ve made and are making to client portfolios because of some enduring changes in the investment environment in the wake of Covid.

Beyond Covid: The Subsidiary Surprises of 2020

The pandemic led to a number of subsidiary events that, in many cases, were more surprising than the advent of the virus itself:

- Delayed and uncoordinated policy choices meant that the US and most of Europe followed the lead of China, an authoritarian state, and shut down vast parts of their economies for the first time, rather than following Taiwan and Korea in keeping their economies more open while deploying extensive testing and contract tracing. In many ways, the policy response to Covid was a bigger surprise than the virus itself and led to so many other extreme consequences.

- Rather than the many months it took the Federal Reserve to respond to the Global Financial Crisis (GFC), by mid-March, the Fed had launched monetary stimulus several times greater than the prior crisis to address credit markets that had frozen as the shut-down threatened a vast number of businesses with insolvency.

- Despite divided government, Congress quickly passed wide-scale fiscal support for workers and businesses. As a consequence, many Americans had the surreal experience of seeing major parts of the economy shut down, while still receiving income either through fiscal support or by working in technology or other professions or managerial jobs that could be performed from home. Online retailing and food delivery, already significant trends, accelerated. Couples and families, competing for space with everyone home 24/7, sought more room, boosting home prices, new home construction and renovation.

- With workers and students cooped up at home, the sickening image of George Floyd being killed by Minneapolis police brought people onto the streets to protest for police reform and greater racial equity across the nation despite the prior lack of significant reform even in the wake of several years of extensive media coverage of earlier police killings.

- Effective vaccines began to be deployed less than a year from declaration of the pandemic, much sooner than most health scientists predicted at the outset and wildly shorter than the normal period for testing and approving a new vaccine. Public disclosure in mid-summer of successful first vaccine trials, followed by FDA approval in December of the first vaccines, was perhaps instrumental in buttressing consumer and business confidence, especially as the first round of federal fiscal support came to an end.

The upshot for US stocks (as measured by the S&P 500) is that they declined 34% peak-to-trough in about a month’s time and would go on to return 18% for the year. By comparison, US stocks fell 57% over 17 months during the GFC and would not recover their prior peak price level for over five years.

The Big Lesson for Investors. The year 2020 illustrates the futility of trying to sell ahead of major market breaks and buy back at the bottom. Even for an investor who thought they saw Covid coming and sold ahead, buying back in time to profit would have been extremely difficult given how fast markets moved and the fear that prevents investors from buying into a falling market, or worse, one that has recently bottomed (and is sure to go down again, they think!).

Adding Value by Rebalancing. Coming back to Taleb’s advice about staying robust, we do this for clients by helping them stay committed to long-term investment policies broadly defined by percentages of cash, stock and bonds. In mid-March, we sold bonds and bought stocks for clients to put them back roughly at their policy allocations. As stocks rallied hard in late spring and early summer, we executed trades to trim the stocks and buy bonds to restore policy balances once again. The extreme nature of market moves then required action across most clients contemporaneously, rather than our normal practice of rebalancing clients in the context of a full study of their cash flow, taxes and other key data in an annual review. We had last taken this step in December 2008 in the depths of the GFC. Since early summer, the continued recovery in corporate bonds has helped keep portfolios more in balance, and we’ve returned to our practice of rebalancing clients across their entire portfolio as we do our deep, annual dive into their financial plans.

To give a bit more detail about these adjustments, we were looking to add quality and durability in our purchase of stocks (since we didn’t know how long the downturn would last), and so we used a Vanguard index fund that tilts toward companies that score better on certain environmental, social and governance criteria and away from resource extraction. As it happens, our purchase was only a few days ahead of the market nadir, and that tilt benefited from the outperformance of technology companies during much of last year compared to the US stock market as a whole. When selling stocks on the way up, we looked to book tax losses, as well as to add quality and economize on underlying fees where we could. The sale of Mairs & Power generally allowed us to book a loss for clients as we incrementally bought back DoubleLine Total Return Bond. Selling Oakmark Global and T. Rowe Institutional International Disciplined Equity likewise booked losses and allowed us to add the lower cost Pax Ellevate fund and an international quality manager in Rajiv Jain’s GQG Partners International fund. Pax Ellevate is a “passive plus” fund with an underlying index that is tilted toward companies with more diversity in their management ranks, a factor that has been shown to add to company performance over time.

The Prevailing Issue: High Debt and Low Interest Rates

Now that major stock indexes have returned to and surpassed pre-Covid levels, how would we characterize the risks and opportunities? And why, if Taleb is right, do we bother talking about the future?

To answer the second question first, we describe the investment landscape and our views to help guide expectations. Not all financial phenomena are random. Tendencies can be observed historically in markets. An easy one is that if interest rates are low, newly issued bonds will have low returns, at least measured over their life. For example, the maximum amount an investor can make from a 10-year US Treasury note purchased at par with a 1% coupon is 1% per year if held to maturity. Another example is that high price-earnings multiples for stocks (a measure of the “priciness” of stocks) tend to provide lower future returns, historically speaking, when measured over subsequent periods of 10 years or more. These observations may affect our recommendations for portfolio positioning, such as the mix of the types of bonds or stocks or other investments to hold. And having reasonable expectations helps investors weather adversity in markets, including by sometimes making other adjustments in life. This is an element in staying robust, or as we call it, “financially fit.”

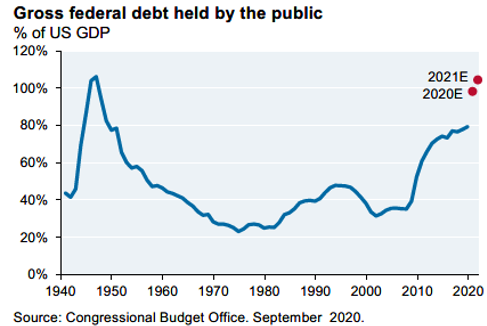

Rising Government Debt and the Federal Reserve’s Purchases of It. To come back to the first question, the most profound feature of the investment landscape is the low level of current interest rates and the swelling of accumulated government debt, thereby causing the political imperative that the yield on government debt remain low indefinitely to keep the cost of servicing that debt from becoming unbearable. Unlike past economic recoveries, the federal government has run a deficit since the GFC. It was hoped that the level of debt accumulation would at least slow to below the rate of economic growth, but without the political will to curb the deficit and then with the enormous spending to offset the economic lockdowns undertaken to combat Covid, it seems federal debt has been pushed to a height that will take a very long time, if ever, to escape.

Note that our country’s past experience with high debt levels, immediately following World War II, was helped by several decades of economic growth significantly faster than it is today, thus enabling the government to grow its way out of debt. Also, the Fed helped by purchasing long-term bonds in the 1950s, thereby pushing down their yield and the interest that the government had to pay. The Fed effectively renewed this practice following the GFC through “quantitative easing” and magnified its purchases in response to Covid. The Fed has also said it would exercise “yield control” if the yield on government bonds gets too high. What amount is too high? The Fed hasn’t said, but if one unsaid purpose of yield control is to keep the cost of servicing government debt manageable, we expect the Fed will not want to see Treasury securities yield more than the rate of inflation. That way, as inflation causes tax receipts to rise, interest on debt below the rate of inflation means that government would be growing its way out of the debt (assuming that it isn’t also piling on new debt through continuing annual deficits).

Given the scale of debt we have accumulated as a nation, especially in recent years, the Fed’s asset purchases seem indispensable. In comments by Federal Reserve Chairman Jerome Powell, minutes of meetings and comments of regional Fed bank presidents, the Fed has made abundantly clear that it will hold interest rates low even in the presence of inflation that at least temporarily runs above the Fed’s 2% target, which may happen in summer 2021 as year-over-year comparisons to depressed prices from the time of Covid’s peak are made. The Fed does not want a repeat of the “taper tantrum” of 2013 when it tried to diminish its purchases, or the stock plunge of late 2018 when the Fed seemed ready to continue hiking rates and diminish asset purchases in the face of economic weakness; in both instances, it was the Fed that adjusted to accommodate the market, not the other way around. Thus, with trepidation that comes with making sweeping statements, we appear to be boxed into low yields on government bonds for as far as the eye can see.

Effect of Low Rates on Investments. How truly low are interest rates? One third of global sovereign debt has a negative nominal yield, and, net of inflation (meaning “real yield”), 75% is negative. Even US investment grade corporate bonds, as measured by major indexes, yield a little under 2% and thus essentially provide no real return. And, that tiny nominal return on government bonds, without getting too esoteric, is really compensation (and paltry at that) for potential changes in market value of long-term bonds when compared to the rock stability of overnight funds and T-bills.

Thus, “the time value of money” (perhaps the most basic concept in finance) has essentially become zero and is going to stay there quite a while. Because the expected return from any investment is the sum of this “risk free rate” plus some compensation for the added uncertainty of the investment, whether it be a stock or bond or what have you (so called “risk assets”), the expected (that is, future) return for all investments has diminished. This occurred as investors bid higher for risk assets and received their current reward of asset price increases.

But just because an investor is willing to pay more for an investment, doesn’t make it fundamentally more valuable; it doesn’t change the stream of interest payments or stock earnings that the investor receives. In effect, outsized current gains caused by a shift in investor behavior are returns borrowed from the future. Likewise, panic selling and the precipitous fall in stock prices like we saw in March is a process of shifting rewards to the future for investors who hold on (or better yet, can buy more). So, in 2020 we quickly went from pushing returns to the future to getting them today. March’s panic selling is long over, but the policy consequences of low interest rates remain.

Low Rates and Financial Planning. It is important to reflect on this dynamic of pushing returns out and pulling them forward because it underlies two foundational elements in our financial planning work with clients:

- We use low and consistent return assumptions in forecasting the path of value of portfolios based on the additional inputs of inflation and savings and withdrawals. Those modest assumptions are appropriate as a matter of caution given the variability in even long-run returns and specifically in an era when, all other things equal, low government bond yields should diminish portfolio returns.

- We spend considerable time talking with clients about their income and expenses, because these are areas where they have some control and can adjust; by contrast, hoping for better investment returns is not a reliable strategy.

Though we by no means relished the selloff, the steep descent gave us an opportunity to “stress test” the assumptions we use to build our portfolio sustainability forecasts, which in turn inform our guidelines about how much clients can withdraw from their portfolios each year without jeopardizing their long-term purchasing power. Even during the lows in March, when we reoriented clients’ forecasts to that environment, we found that our guidelines were still appropriate. This was a battle test of a crucial element of our planning for clients, because portfolio sustainability lies at the nexus of investment counsel and comprehensive financial planning. In the absence of this forecasting exercise, we might instead be encouraged to look to often volatile and expensive investment products, or potentially counter-productive trading (as opposed to orderly, procedural rebalancing) in response to extreme market stress. Or said another way, we planned for a market surprise like this, and we’re pleased to report that the plans held.

Economic Situation: Reasons for Optimism and Concern

With low rates as the backdrop, the present investment environment is one where there is considerable reason for economic optimism. That optimism is reflected in high prices for most assets, but there are some better values in areas away from Fed stimulus and among companies that have not prospered from the “work from home” trend. Reasons for economic optimism abound:

- Significant slack in the labor market provides opportunities for hiring that can lead to greater production so the economy can regain and grow past its prior peak.

- In particular, significant pent-up demand for dining and travel will be unleashed as inoculations increase, helping to put hospitality and travel workers back on the job.

- A sizable fraction of stimulus money was saved by households, so they are in a better position to spend when the abatement of Covid gives them a greater chance to do so. However, in the long term consumers may save more after the second big recession in a generation. Additional stimulus is being delivered to households over the next several weeks, and President Biden has asked for significantly more. The cumulative effect of reopening the closed portions of the economy and additional stimulus should result in very brisk economic growth in the absence of other closing activity.

- Covid foisted some additional costs on firms, caused the failure of thousands of small businesses, but also accelerated trends that may lead to greater innovation and productivity. Numbers of new businesses registered with the IRS increased markedly beginning in the summer, which was refreshing after several years of decline.

- Corporate bond defaults, a reliable indicator of economic stress, appear to be peaking.

The big near-term risk with the economic situation has do with continued problems with the rollout of Covid vaccines or mutation of the virus in ways that thwart the effectiveness of current vaccines. We’ve had some bumps with the vaccine rollout and signs of mutation already; worse problems could derail or delay the recovery.

There are also larger structural issues that are concerns emanating mostly from the political arena:

- High corporate profit margins (and thus, high stock prices) have been enabled by mergers, lax antitrust enforcement, low interest rates, low tax rates and subdued wages. Apart from interest rates, all of those may be changing. President Biden would like to increase the corporate tax rate from 21% to 28% and broaden the base; the resulting change is projected to cost 10% of S&P 500 profits. Antitrust enforcement has moved up in recent years, a welcome development for consumers and the economy in our view. As an example, Google has become a target of both federal and state lawsuits related to its exclusive payments for search. A portion of Google’s labor force recently unionized, perhaps a harbinger of greater union power in an economic sector where unions haven’t played much of a role. The Atlanta Fed wage tracker survey shows wages rising about 3.5% for workers who remain employed. That rate of increase didn’t really drop with the recession, perhaps due to pervasive reports by businesses of their difficulty finding appropriate labor to fill jobs, as we address below in more detail.

- The US has had a heighted degree of political division for some time, but the stark difference of belief about the basic facts of the outcome of the 2020 election, culminating in the sacking of the Capitol building by a mob intent on overturning the election was incredibly shocking and dispiriting. We tend to take our government for granted and think of political risk as something one encounters only in emerging markets. The storming of the Capitol was a manifestation of real risk of instability at the core workings of our democracy. We hate to think we are witnessing the irreversible decline of the United States, but clearly we have a great deal of repair to undertake. Even in the past several years, foreign ownership of US Treasury securities has dropped. Are perceptions of political risk partly to blame?

- Our national struggles with economic inequality have been made significantly more difficult due to Covid. And some of our policy responses may make the situation worse in the long run.

Economic inequality in the US has moved in waves over many years. The most recent increase began a few decades ago while trade in goods accelerated, allowing developing nations a greater share of the global economic pie. During this time, technology businesses became incredibly profitable using little invested capital and modest numbers of employees. The technology workforce and the professionals that supported them became well paid and essentially shrank the middle class by moving up out of it, while the rest of the economy seemed largely designed to cater to their spending habits. As unemployment neared 3% before Covid struck, wages for the lowest income Americans had finally started to grow faster than for higher income groups, an encouraging sign.

But as Covid took hold and the economy was shut down, the travel, hospitality and retail sectors were hit the worst. Women and persons of color, being disproportionately represented in those sectors, suffered the highest rates of unemployment. And throughout the economy, with schools mostly shut, women left the workforce in large numbers to manage children’s remote schooling. Federal unemployment assistance (in addition to normal state unemployment insurance) has helped, but it is temporary. Like residential construction workers after the housing bust who needed to be redeployed elsewhere in the economy, we should expect the same of many of these workers. The US is short in technology workers and many skilled trades. We would hope that at least some could be retrained in these desirable areas. Also, our infrastructure is badly in need of repair and we have to continue developing renewable power to complete our transition to cleaner energy. The federal government could deploy significant numbers of permanently unemployed people through a reprise of the Works Progress Administration of the 1930s if we also streamlined permitting for projects so they could move forward. Finally, we could concentrate additional STEM education resources in urban low-income neighborhoods to strengthen communities and help meet demand for workers.

What hasn’t lessened inequality is the renewal of the Fed’s zero interest rate policy. Low interest rates have boosted asset prices, notably stocks and housing, making well-off Americans more well-off, while those without assets now must save more for a house or their retirement. As well, Uncle Sam sent stimulus dollars indiscriminately to every household below certain income levels regardless of their employment situation. The ease with which this has been done twice, and may be repeated a third time if President Biden’s bid for additional stimulus checks is approved by Congress, may reflect a new dynamic with some adverse side effects. We wonder how our federal fiscal imbalance can improve if the great bulk of citizens can make increasingly easy claims on a public fisc that is fed largely by a small number of high-income earners. We also wonder whether the supplemental federal unemployment compensation elements of the stimulus bills are harbingers of a “universal basic income” benefit, something that was a fringe idea until recently and not even widely adopted in Europe, which has a wider social safety net than the US.

Tactical Investment Views

As clients know from their work with us, we consider this backdrop not with a view to making dramatic changes, such as exiting or entering the stock or bond market altogether, but from the standpoint of how best to position clients within the investment policies (of stocks, bonds and cash) that they have selected. Consistent adherence to policy or a gradual adjustment thereof (say, due to the advent of retirement) is a critical discipline in the pursuit of financial fitness and particularly in avoiding the error of a dramatic change.

Bonds. As described above, most government bonds offer very limited nominal returns and negative real returns. Even investment grade corporate bonds (i.e., those rated BBB and above) offer negative real yields. Thus, earning actual real returns in bonds means taking on credit risk through “high yield,” floating rate debt, emerging market debt, commercial mortgages, private lending pools and the like, which we refer to as “peripheral” bonds. Given the choices of going without significant yield, buying more stocks to seek higher returns or using alternative strategies for bonds, in many instances we believe it is worth taking the greater market and illiquidity risk with portions of a client’s bond investments that will not need to be sold to purchase additional stocks in a period of severe decline. Thus, we distinguish these peripheral bond sectors from the high-quality core bonds that are the biggest portion of client bond investments and were used to purchase additional stocks in March.

Peripheral bonds have always been part of client portfolios, but we are exploring them more widely, including by accessing them through structures other than mutual funds as a means of seeking reliable current income for a portion of the portfolio that can stay invested long term. Depending on one’s objectives, these alternative fixed income investments are worth pursuing for their own purposes. But another way of viewing them is as a “least worst” avenue for an investor who, likely due to circumstances related to their reliance on return from their portfolio to meet current household needs, cannot easily wait out the significant periods (sometimes 10 years) for stocks to provide positive cumulative returns. Thus, such an investor needs additional return from the bond portion of their portfolio (rather than having it serve only as a stable reserve) and prefers not to take the other major avenue—investing more deeply in stocks—which involves more fundamental risk of uncertainty about valuation and near-term return. We recommend that clients refer to the attachment to this letter (Identifying and Distinguishing Among Risks) for more information on these structures and for descriptions of the relevant risks, which are important to understand.

Despite our view that better yield should be sought away from government bonds, there is still no substitute for durable, high quality “core bonds” in a portfolio in sufficient quantity to play at least two roles: (1) to be available to sell with little loss or potentially some gain to purchase more stocks when stock prices fall; and (2) as a source of cash to tide over an investor if necessary while stock prices recover, potentially over a number of years. For this purpose, we have used DoubleLine Total Return Bond Fund, which is concentrated in mortgages, and we are happy with the results. Although a fund following the Treasury bond market (and by extension the major bond indexes) would have had a higher return for the year, Treasuries being lower in yield and longer in duration have more risk of price moves from changes in bond yields. DoubleLine remained stable during the March downturn, whereas Treasury prices became quite volatile. From here forward with rates only really having room to rise over the mid-to-long term, we are happy for the lower duration of the mortgage market.

Stocks. Many investors may regard the US stock market as quite high, but the situation is more mixed than it appears at the surface. As mentioned early in this letter, some companies have benefited tremendously from the bulk of the US labor force having to work from home (WFH) because they are the vendors of the technology systems that make remote work go, whether that is cloud storage, customer management systems, video-conferencing or the like, while others have benefited from shifts in consumer behavior (e.g. fewer gym memberships and more purchases of gym equipment; less travel and dining out and more spent on home appliances and remodeling). While people have been stuck at home and perhaps looking to use some of their stimulus money, individual interest in the stock market has mushroomed, as is evident from the dramatic increase in the number of individual stock brokerage accounts, investor sentiment surveys, and interest in initial public offerings and special purpose acquisition companies (“SPACs”). (In case you’ve heard of SPACs and wonder what they are, you might think of them as one-company buyout funds where the SPAC does an IPO to raise cash and later purchases the shares of a single private company (or a public company in need of cash) and thereafter trades as a public company with a portion of the shares held by the promoters in exchange for their organization and management efforts.)

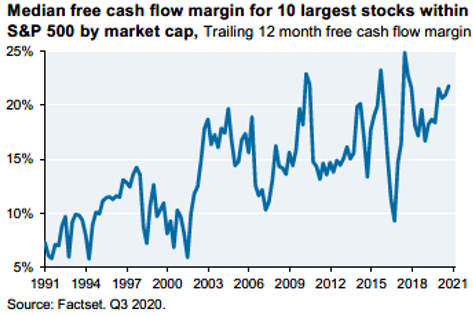

Despite these signs of excess, many other parts of the US stock market are more reasonably priced than the top technology companies that attract so much attention. And the biggest stocks have a cash generating ability beyond prior eras as shown in the chart to right. Having said that, essentially all of the stock market is priced for a smooth recovery. Investors are looking over the remaining canyon of lower corporate earnings for companies whose businesses are still constrained by Covid. In some sense, this investor behavior is admirable in that investors should take a very long view of their stock ownership. On the other hand, the optimism makes the market more fragile to disappointments, such as a delay in the completion of nationwide vaccinations.

With this backdrop, we’ve sought to tilt client stock investments toward better value or more durable companies or toward long-term growth trends as follows:

- Approximately half of all client stock allocations are to foreign markets where prices are significantly lower and where, with emerging markets, growth rates are higher. The large and growing US trade and fiscal deficits should put continued downward pressure on the dollar, and, if so, then these investments likely will have a tailwind of currency appreciation behind them.

- Given how quickly the political environment, and social reaction to that environment, is changing, such as corporate reaction to the storming of the Capitol, we believe companies need to be diligent in managing their “social risk.” We are glad to have previously adjusted portfolios toward some managers and passive index funds that give more careful evaluation of environmental, social and governance (ESG) risks. We also expect the flow of increased investment dollars toward ESG strategies and related opportunities to continue for a long time (similar to the long trend toward passive investing). Our work in this area is fundamentally about risk-reward assessment, although for clients with social-impact objectives for their portfolios, they may be especially glad for these investments.

- We like the “picks and shovels” approach we’ve largely taken to the increased business investment in sustainability technology as represented by client investments in Pax Global Environmental Markets. In the short term, as the price of oil recovers with the economy, clients may miss a little bit of return from traditional energy companies, although they are now only 3% of the US stock market. We expect the trend of dollars moving toward sustainability technologies to continue for a long time. We are also exploring means of further investment in renewable infrastructure, although some of it is quite low risk-low reward that is not attractive, and other parts are accessible only through illiquid private structures.

- Over the last several years, we have increased the passive index component of stock investments as our view of the cost-benefit tradeoff in individual managers has evolved. At the same time, the biggest companies in the US stock market have garnered an increasing share of returns. This concentration effect has benefited investors, because passive investments (currently dominated by growth stocks) help keep clients invested in companies that are performing well, when the natural behavior of investors (even many managers) is to take profits early in such companies by selling. At it happens, clients have also benefited from outstanding performance by growth stock managers. While we keep an eye on these exposures, we are not inclined to cut back allocations to growth much below a normal rebalance of a portfolio toward model positions (i.e. among US vs. foreign, and growth vs. value) because as clients know from working with us, we don’t make extreme calls on exiting and entering core assets classes, which would include growth stocks, and in any event the environment for growth stocks remains compelling. Covid has accelerated economic trends that were already in motion, driving change in an economy that has grown slowly in recent years compared to historical averages. Thus, companies that can deliver consistent, above average growth deserve better valuations, especially in a low interest rate environment that is likely to persist for a long time. Occasionally we expect that the enthusiasm for growth will get excessive and the rebalancing process will help clients reap the attendant rewards by putting some of that value back toward other parts of the portfolio.

The Year at KBBS

As it was for all of you, 2020 was a year of challenges and adaptation for us personally, in addition to collectively as a firm. All of the principals had their children at home, either because of their youth, absence of in-person schooling, return from college or refuge from the big city. Among our colleagues, there were losses of a father and a mother, the birth of a grandchild and a few home relocations. Cam even took her family on the road for several weeks of remote work and schooling while seeing many natural wonders. More so than at any other time in this author’s memory, life was lived extemporaneously, and despite the losses there were unexpected blessings also. We hope the same was true for you.

We’ve written before about our transition to working remotely as a firm starting in early March. This situation has worked well given secure links between Schwab and our office and secure remote connections we all enjoy to the office. We do have staffing at reception and mail collection that enables us to deal with an actual paper situation or rare client appearance, and we’ve even handled a couple of curbside document signings. Clients have handled remote meetings via web conference or phone remarkably well, and we appreciate the spirit of adaptation that we’ve undertaken together.

We are in the process of integrating new software tools to assist with managing client portfolios. Those tools include a client portal that we hope to start rolling out in the second half of 2021. The portal will include visualizations beyond what is available at Schwab and should be a more streamlined process for exchanging confidential documents and obtaining non-Schwab data (such as 401(k) investment values) than clients currently experience.

When immunity to Covid is pervasive, we will return to the office, but will keep remote work available to all of us as needed and likely collectively work from home certain days of the week. In that sense, Covid has helped us explore some options that have benefits for both us and our clients. We also look forward to traveling to see clients as the health situation permits; we always appreciate seeing clients in their homes and benefit from seeing other parts of the country.

The year also was one of growth through additions to our team. Austin Jodrey, originally from Maine, joined us after a few years of experience in support and administration in a major insurance company and having become a Certified Financial Planner certificant. Blaine Thompson is a Seattle native and more recently out of college, and joined us after earning his Masters in Finance and work experience in both stock brokerages and private equity. We are excited about the contributions that they are making to the firm.

Colleagues Kyle O’Connor and Gianna Giusti continue their growth in the firm through increasing leadership on client matters, additional education, key roles in trading and compliance, respectively, and by training and supervising our newer colleagues. And assistant Raylynn Branes is back at the firm full time after several months assisting her mother through the end of her life.

The end of 2020 marked the retirement of Ted Kutscher, our founding partner and principal, from regular responsibilities in the financial planning business, as has been planned for some time. Ted will forever be a member of our team as Principal Emeritus and continues his regular contact with all of us through his estate planning and other legal work for many of our financial planning clients, which had become the focus of his work as the financial firm grew in size, specialization and capability. Ted continues as well as a source of counsel on key issues for the firm and clients. We’ve referred to Ted as our “cultural polestar.” All of us are committed to the values of service, integrity, effort, curiosity and humility he employed in establishing the firm in 1991. We are grateful for his leadership and development of the firm and of all of us personally, and we wish Ted the rewards of increased time for family and other endeavors, even as his legal work continues.

Thank you for your confidence and trust in us. We look forward to earning it again and again.

Kindest regards,

Scott D. Benner

Cameron J. Barsness

Ryan V. Stevens

ATTACHMENT A

Identifying and Distinguishing Among Risks

Types of Risk. As we counsel clients to invest in bonds, stocks or other assets, it is important to separate the kinds of risk represented by each of them, both as to type and magnitude. For each client, our job is to construct a mix of assets that involves risks that are compensated in return, but in the aggregate are not greater in a period of market stress than what a client can bear. Most risks fall into the following categories:

- “Fundamental risk” is the uncertainty that a payment stream will be realized as forecast or promised. With bonds, this risk is called “credit” risk. With stocks, fundamental risk is the uncertain nature of the income that a company will earn over time or perhaps pay out as dividends or buybacks. In both cases, the risk is real apart from any change in investor views about the risk. The bond will be paid or not; the company will earn the forecast amount of income or it won’t; time will tell. Since bondholders are entitled to payment ahead of stockholders and are (usually) promised a fixed stream, there is typically far less fundamental uncertainty in a bond than in a stock. Fundamental risk for a portfolio is reduced by diversifying investments, whether stocks or bonds or both, among a number of companies. Still, the greater uncertainty about corporate earnings than bond payments explains why the range of possible returns in a portfolio increases as stocks are added and bonds reduced, a risk that is magnified through trading activity for investments as described below.

- “Market risk” is the risk that the observable market price for a security traded in an organized market will change based on changes in investor views about the value of payments represented by the security. Most often, those changes might be specific to changes in perception about whether the stream of income from the investment will be realized in the amount previously anticipated. Market risk is distinguished from fundamental risk because changes in investor perception will drive changes in value (at least temporarily), regardless of whether the anticipated change ultimately occurs. This risk is most prominent with stocks because there’s so much opportunity for investors to change their views about what the ultimate rewards for holding the stock might be, especially for “growth stocks” where the rewards are projected to come from increased sales and profits in the distant future.

All investments also have varying degrees of risk of changes in value arising from actual and anticipated changes in general interest rates or other economic phenomena. As described in the above newsletter, general interest rates are a fundamental input in the valuation of all investments. This is known as “duration risk” and tends to be greater with assets whose payment streams reach far in the future, such as growth stocks and long-term bonds.

Changing investor views about the economy can drive major moves across entire stock and bond markets. This was seen most prominently in March when stock prices generally fell by 37%. Covid is a horrible event and the shutdown of the economy has caused huge dislocation for many firms and cost many jobs. Nevertheless, we are moving through it. The S&P 500 is forecast for 2021 to exceed its earnings for the year 2019. For 2020, earnings are forecast, when 4th quarter earnings are reported, to be off less than 20% from 2019. Even if these forecasts are a bit too rosy, it is easy to see how markets tend to overshoot fundamental values when emotions are running hot. And diversification across companies and even geographies diminishes in utility with the selling pressure because investors who need to sell (perhaps to pay back a loan) will eventually reach for any asset they can sell; thus, selling pressure can become contagious and self-reinforcing. During March, even the price of gold, a classic haven in times of stress, declined.

Market risk is best handled by having enough cash set aside or generated as reliable income through employment or yield on a portfolio, to support an investor through periods of market stress. That is why we are so focused in our planning process with clients to understand and forecast their need for cash and set aside reserves prior to making portfolio adjustments.

- “Illiquidity risk” arises from the absence of a regular daily trading market for an investment or perhaps limited rights to redeem from a fund. For example, real estate is an illiquid asset because the unique nature of every parcel means it can’t be traded in a daily market unless packaged and grouped into a fund (called a real estate investment trust, or REIT) and securitized into shares, which can then be traded on a stock exchange.

An individual real estate parcel (or even an entire REIT) may have low fundamental risk of the underlying income stream depending on the quality of the real estate and the creditworthiness of the tenants. Other examples of illiquid assets are private equity and private lending funds. These have varying amounts of underlying fundamental risk depending on the nature of the assets they hold.

Thus, an illiquid asset isn’t necessarily fundamentally risky; one has to pay attention to the nature of the asset. But it is certainly true that the illiquid nature of an asset means there is additional risk of loss if the investor may need to sell the asset prior to its maturity or other than through the ordinary process, which might be lengthy (as with real estate). Consequently, we recommend illiquid assets only under circumstances where the asset would not need to be sold in a period of market stress. In that instance, a client can often receive incremental return not available for a publicly-traded investment of a similar type.

Since real estate isn’t publicly traded, the changes in market value are often opaque to owners other than true professionals. The websites Zillow and Redfin try to make up for this by using algorithms that employ recent sales, listing prices and other factors to estimate current values of residential real estate. But stated more generally, illiquid assets are subject to changes in fundamentals or valuation inputs (e.g. interest rates), but their owners may be shielded from (or denied of, depending on one’s viewpoint) the ability to readily view the changes in value that would be observable if the asset were traded daily.

For any illiquid investment, a secondary, private marketplace of participants typically exists that may be accessed through brokers and loose networks. Thus, many illiquid assets can be sold within a reasonably short time, but typically at a discount to fundamental value, sometimes a steep one. The sums are usually large and require knowledge of assets for which there is no public information; consequently, there are typically few bidders. This works to investor advantage as well when the investor participates in a fund that purchases illiquid investments in this discounted manner.

As mentioned above with REITs, an illiquid asset type can be made liquid (that is, publicly traded), when it is bundled into a fund whose shares are publicly traded. Another example is “business development companies” or BDCs, which invest in private company secured loans (an illiquid asset type). BDC shares are often publicly traded and are a type of “closed end fund” (or CEF) meaning that the fund has a fixed number of shares that investors buy or sell through a stock exchange, rather than by contributing cash to or withdrawing cash from an “open-end fund” such as a typical mutual fund. REITs, BDCs and other CEFs can be an excellent means of investing in an asset category that is otherwise difficult for investors to access, either at all or in a diversified manner. And the closed-end nature of the fund may make it a better means than a mutual fund for the manager to manage the underlying assets (especially illiquid assets) since the manager doesn’t need to lay aside cash for possible investor redemptions. But investors need to recognize that such funds’ shares are more volatile than the underlying investments because the public trading market for the fund shares means that changing investor views will more dramatically affect the trading price of the shares than the value of the underlying assets. This drives changes in the degree of discount or premium that the shares of the fund trade at relative to their net asset value (NAV) per share. CEFs also usually employ leverage, which has the effect of magnifying fundamental changes in the net value of the underlying asset portfolio and subjecting the fund to changes in value from changes in interest rates. CEFs may be appropriate to hold for their enhanced yield or other reasons, but investor need to be prepared to continue holding them through periods of market stress the same as with stocks.

Some funds holding private assets offer investors rights to redeem, but these are often limited if investors collectively seek to redeem more than a certain fraction of the fund at one time, say 5% of the fund’s value in any calendar quarter. This open-end nature is an attempt to offer investors the opportunity to invest in the underlying asset category without the extra volatility from exaggerated swings of investor perception that effect CEFs. Instead, the fund’s shares for purchase or redemption will be valued at the net asset value of the underlying assets. Thus, comparing CEFs and private open-end funds, CEFs allow a ready sale, but at a significant discount to NAV (often 15% or more) during market stress, while open-end funds during stress may lengthen the period for redemption, albeit at the NAV per share. In either case, with private funds or CEFs, investors need to be prepared to hold the asset long-term as they would with stocks.